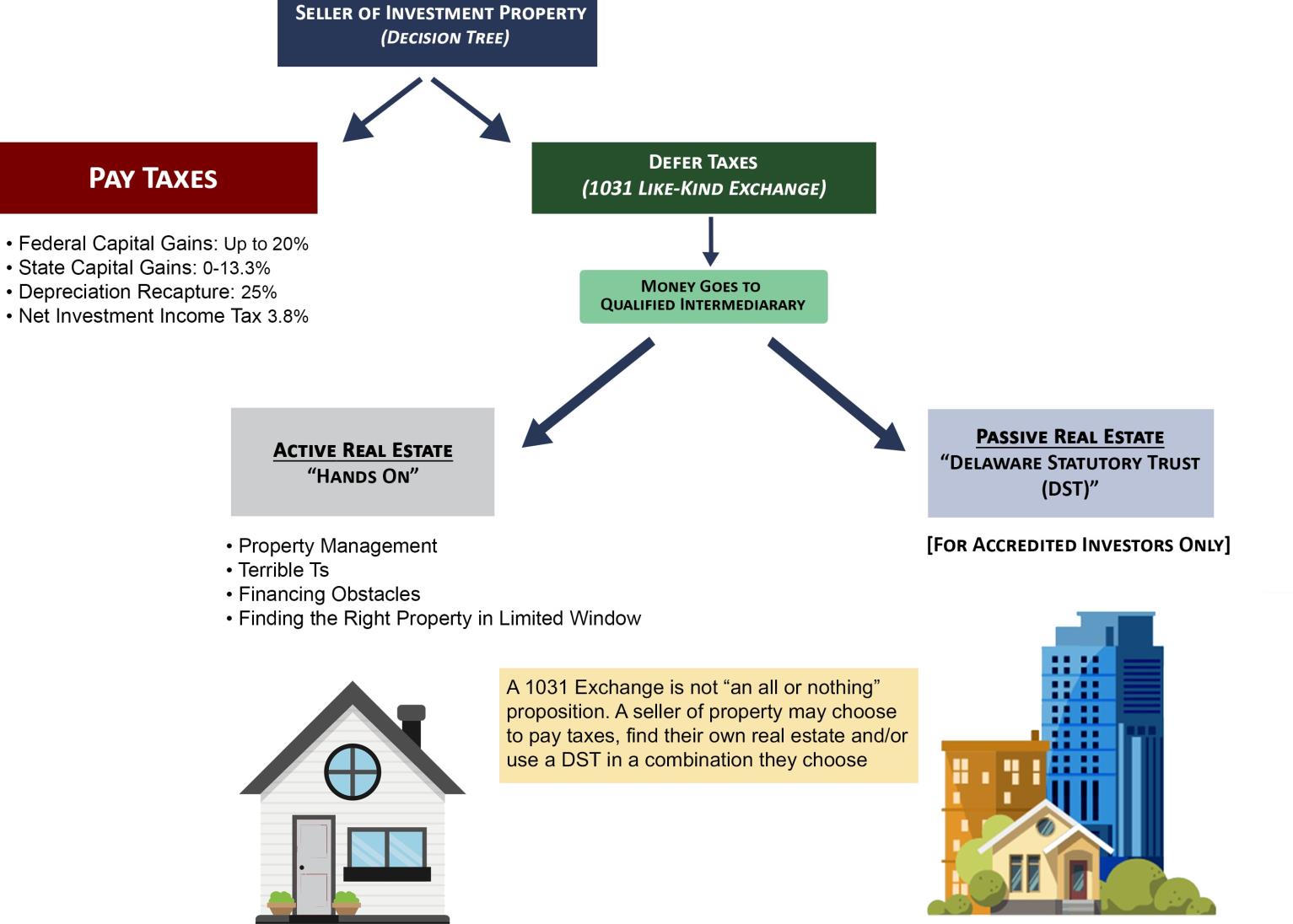

USING A DELAWARE STATUTORY TRUST TO COMPLETE YOUR 1031 EXCHANGE

In the majority of cases, 1031 Exchanges are completed by the investment property owner with the help of a real estate broker. However, if suitable, there may be another alternative – a passive solution to satisfying a 1031 Exchange – and that is a Delaware Statutory Trust (DST).

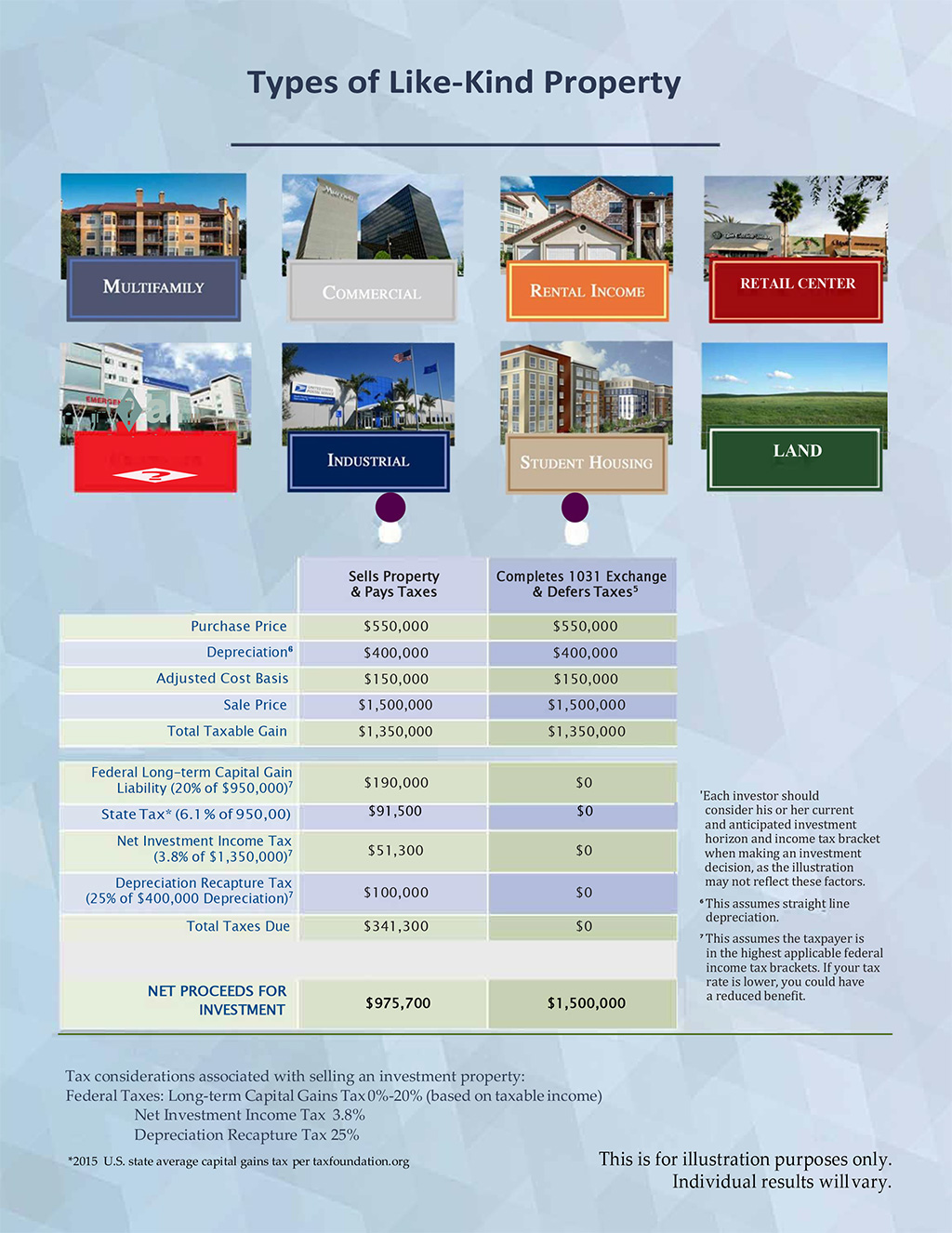

DSTs that are properly structured are recognized by the IRS as qualified replacement property for real property. Investors in a DST are not direct owners of the real estate. The trust holds title to the property, for the benefit of many investors, each of whom has a “beneficial interest” and is treated as owning an undivided fractional interest in the property.

Simply put, DSTs provide a turn-key solution for investors who may not have the time, energy or real estate expertise to find and/or manage a replacement property. DSTs can be used for all or a portion of the sales proceeds. Also, be mindful that there may be fees and expenses associated with a DST.

With its unique structure, a DST can offer you many potential benefits:

- Access to institutional-quality real estate

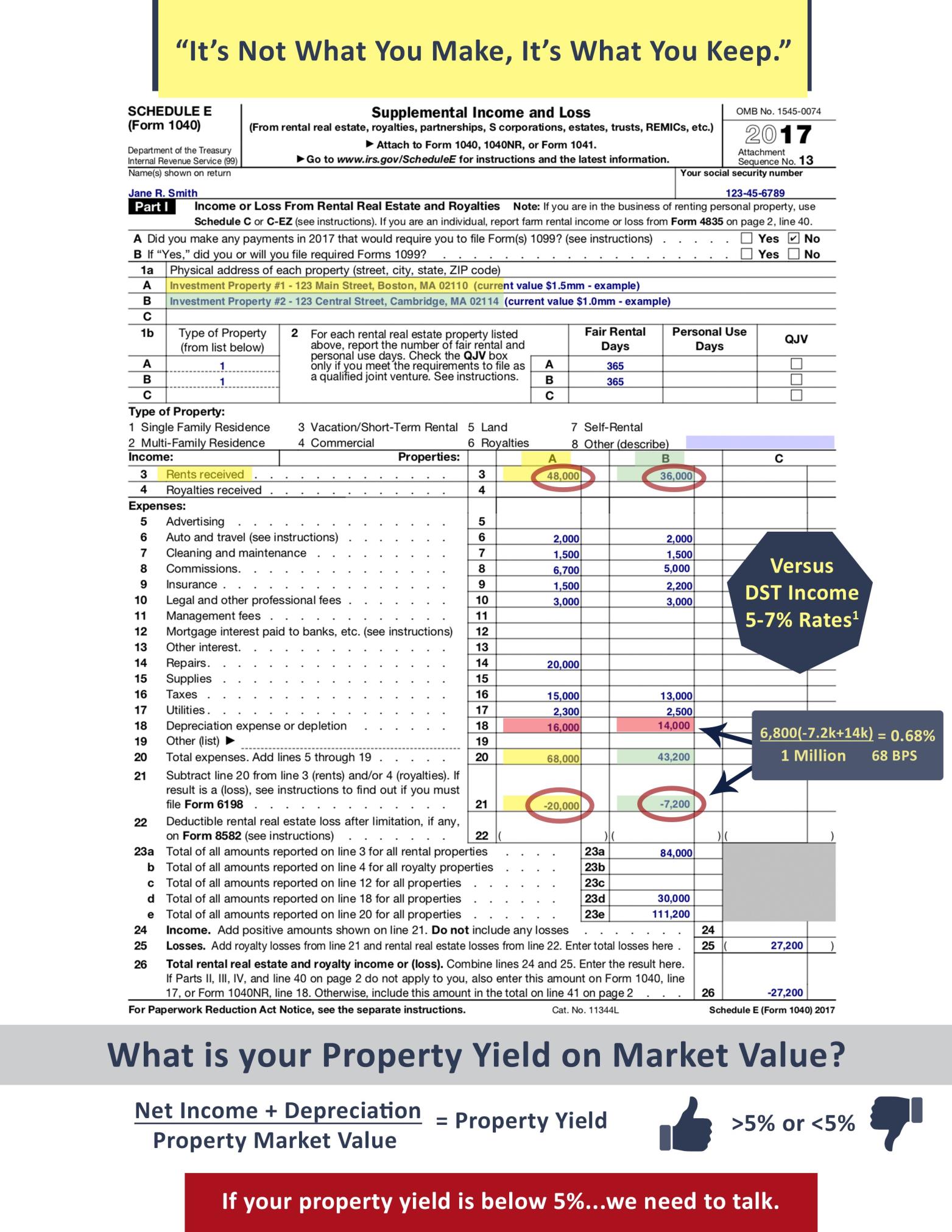

- Professional asset and property management

- Passive ownership

- Non-recourse institutional financing

- Lower minimum investments

- Portfolio diversification

- Ability to close quickly

Guidelines For DSTs

There are certain guidelines that DSTs must follow. Specifically, a DST may not:

- Invest accrued cash, from rental income or investment proceeds, between distribution dates in anything other than short-term securities

- Accept additional capital to the DST

- Renegotiate terms of debt or enter into new financing

- Renegotiate leases

- Enter into new leases (except in certain circumstances)

- Make improvements other than minor non-structural repairs

We offer a complimentary appointment available to discuss your property and review your tax return and discus your options. A diversified portfolio of DST properties can eliminate property management and potentially increase your monthly income and reduce income taxes. It’s worth a visit to find out.

It is important to note that DST investing is subject to specific eligibility criteria, and only individuals who meet the definition of an accredited investor are permitted to participate.

DST 1031 properties are only available to accredited investors (typically defined as having a $1 million net worth excluding primary residence or $200,000 income individually/$300,000 jointly of the last two years; or have an active Series 7, Series 82, or Series 65). Individuals holding a Series 66 do not fall under this definition) and accredited entities only. If you are unsure if you are an accredited investor and/or an accredited entity, please verify with your CPA and Attorney. Before considering a DST investment, it is crucial to evaluate your eligibility as a qualified investor. Our team is committed to assisting you in this process, ensuring that you meet the necessary requirements to participate in DST opportunities. Additionally, we are here to address any questions you may have and provide detailed information to guide your investment decisions.

Please be aware that DST investments involve risks and considerations which include but are not limited to substantial fees and expenses, inability of the DST to actively manage the property, strict timing limitations and risk of not meeting requirements for 1031 exchange tax treatment, and other negative tax consequences. There are risks associated with investing in real estate and Delaware Statutory Trust (DST) properties including, but not limited to, loss of entire investment principal, declining market values, tenant vacancies, lack of liquidity with restrictions on ownership and transfer. Potential cash flow, returns and appreciation are not guaranteed and could be substantially lower than anticipated. Diversification does not guarantee profits or protection against losses.

Additional risks and considerations related to investing in 1031 DST commercial real estate include, but are not limited to, general real estate risks, financing risks, tax risks, interest rate risk, management risks, operating risk, market risks such as supply and demand, changing market demographics, tenant turnover, tenants inability to pay rent, acts of God such as earthquakes, floods or other uninsured losses. There are also potential risks relating to the trust structure and the potential for adverse changes in laws and regulations. This material is not to be interpreted as tax or legal advice.